.svg)

.png)

.svg)

Table of contents

- Coffee Dead End

- What are Behavioral Design and Nudges

- Basic example: how nudges help prevent loan delinquencies

- 5 reasons why it works

- 5 reasons why it doesn't work

- Results and prospects

Coffee Dead End

Feelings of guilt, shame, and fear are the eternal companions of financial issues. Why?

Consider the situation: you walk into a café, see that your favorite coffee costs $10, and decide to walk away. There is no coffee; an unpleasant aftertaste remains.

Situation number two: the same thing happens, but you decide to take a coffee, and now you're sad with the coffee. There is no money, and there is also an aftertaste.

We think the choice is between buying and not buying, but it’s really about guilt, the desire to be responsible, and the longing not to deny ourselves small joys. This is where behavioral design comes in.

What is Behavioral Design?

Behavioral design helps people make better decisions by shaping their environment.

If this still sounds too abstract, let’s clarify it using an example from a well-known company — Duolingo. Its mascot encourages you every day with friendly messages and playful reminders. The app motivates you to learn languages.

Behavioral design uses a tool called a nudge.

You might think this sounds manipulative — that someone is telling you what to do.

In fact, these tools contribute to a sense of control and stability, especially in the financial sector.

Important: A nudge is not an alternative to basic tools such as financial education, legal protection, or flexible terms.

It complements, facilitates, and activates them. Without a solid foundation of transparency, fairness, and accessibility, nudges become empty gestures.

Basic Example: How Nudges Help Prevent Loan Delinquencies

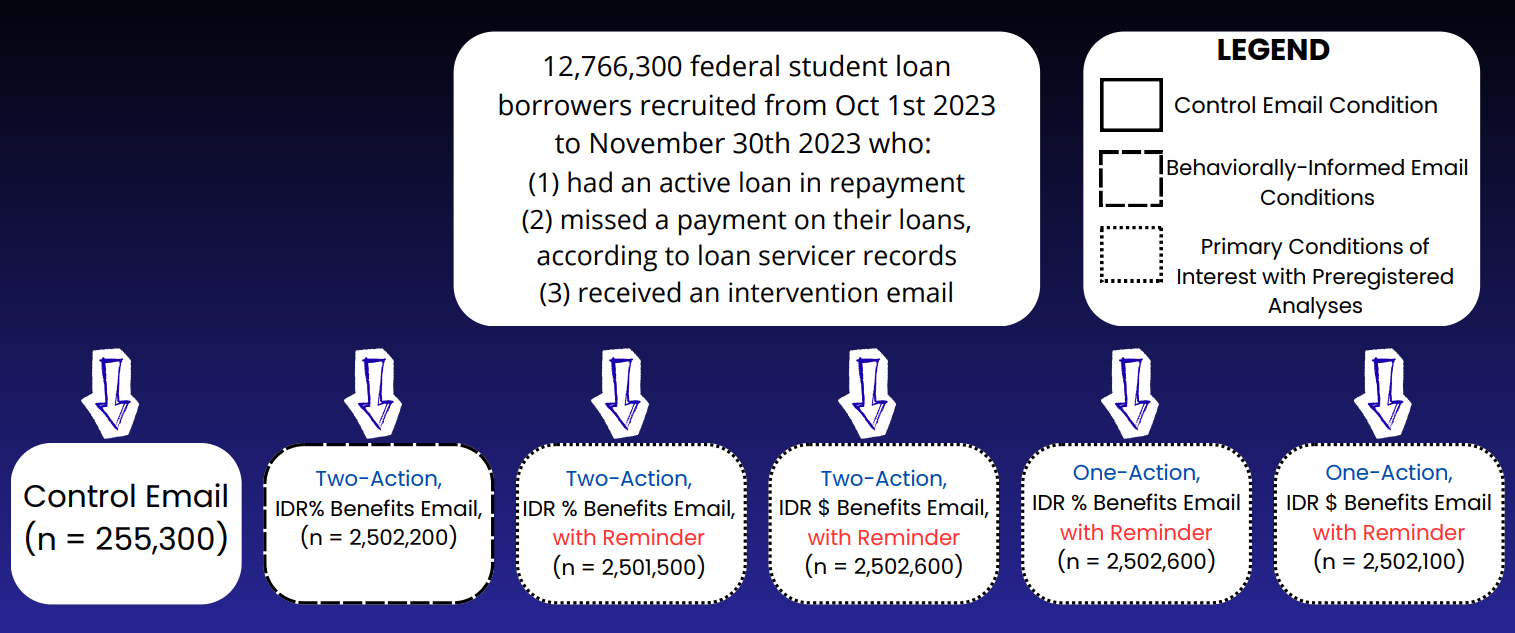

A recent study titled Behavioral Nudges Prevent Loan Delays at Scale (PNAS) illustrates how such “soft nudges” can help people in financial difficulty.

In the United States, student debt exceeded $1.5 billion in 2024. Through the efforts of the study’s authors and the U.S. government, over 13 million people participated.

The researchers focused on a large-scale challenge: how to help borrowers avoid delinquencies on loans — not through harsh penalties, but through behavioral interventions.

Key issues identified:

- Procrastination: putting off decisions.

- Friction: complicated or bureaucratic processes.

- Passivity: belief that problems will solve themselves.

- External factors: political or economic crises.

Based on this, the researchers asked: can nudges encourage more people to sign up for payment plans (income-driven repayment, automatic debit), thereby reducing delays?

They tested several types of prompts. Participants received structured emails about overdue debt, with three main differences:

- Reminders: behavioral science–based emails and notifications.

- Framing: benefits presented not just in dollar amounts, but in percentages.

- Combination of actions: motivating two behaviors at once (e.g., sign up for a plan + enable automatic payments).

The table below shows all the variations of the notifications sent.

Results: Behavioral emails reduced loan delinquencies by 0.42 percentage points within 60 days.

While seemingly small, this difference is significant at scale. Repeated reminders increased the reduction to 0.57 percentage points.

3 Reasons Why It Works

- Transparency: simple setup with minimal clicks and bureaucracy.

- No pressure: “Most customers are already saving 10%” — a positive social cue.

- Sense of achievement: “I activated the debit,” “I didn’t forget to pay.” Small wins build momentum and confidence.

3 Reasons Why It Doesn’t Work

- Pressure resistance: a commanding tone (“If you don’t start saving 5% today...”) triggers resistance.

- The problem goes deeper: saving 5% doesn’t help if that 5% covers essentials.

- Ignoring context: “Neighbors save energy” works in cultures valuing comparison, not universally.

Results and Prospects

The PNAS study shows that large-scale improvements can come from simple, thoughtful interventions — without pressure or penalties.

Behavioral design is not a cure-all for financial problems, but it restores a sense of control and calm in a world often ruled by anxiety and guilt.

Its strength lies in simplicity, support, and transparency — not to force, but to guide.

When nudges respect choice rather than apply pressure, they become instruments of care, not control.

That’s when financial behavior stops being a source of shame and becomes a step toward peace of mind.

.svg)